VIDEO TRANSCRIPT

This is Neil Portus from Tailored Partners. I work as a freelance CFO for growth companies. This video is for startup founders & SME business owners to show them how to build a financial forecast and set investor expectations for their first fundraise. I’m going to walk you through my “1-5-10 Framework.” Let’s dive in!

My 1-5-10 Framework:

Year 1: Keep It Achievable

Years 2-3: Demonstrate Scale

Year 5 (+/- 1-2 years): Deliver Results

Year 10: Change The World!

MY 1-5-10 FRAMEWORK

Okay, the 1-5-10 in my framework refers to Year 1, Year 5 and Year 10 of the forecast.

Year 1

Starting with Year 1, I call this “Keep It Achievable.” I think the key here is the make the Year 1 forecast something you are confident you can achieve because you don’t want investors to be disappointed right out of the gate. There are always unforeseen challenges right after a fundraise so give yourself margin. Investors will focus more on the Year 5 numbers where they are looking for their return & we’ll touch on that shortly. But I have seen forecasts that are best case and frankly too optimistic in the first year which led to investors being disappointed right from the start and a company’s founders playing catch up from the get-go. So, focus your investors attention on the on the Year 5 forecast & give yourself something you can achieve in Year 1.

Years 2-3

OK before we get to the Year 5 forecast let’s look at Years 2-3 and I call this “Demonstrate Scale.” This is the bridge from the achievable Year 1 forecast to the Year 5 forecast that will deliver on what your investors want. The key to this section is that the model should show how the business will scale here. For example, how user acquisition will accelerate or economies of scale will develop. Know the key metrics that you’ll want investors to focus on and let those be the ones that you benchmark against. Pick measurable ones which show business performance; not too many though to keep the messaging as simple as possible.

Year 5

Next is Year 5 which is the most important part. I call this “Deliver Results.” This is the time frame when investors will be looking to realize their return. Here, it’s vital that you research and understand WHO your target investor is and know WHAT return they’ll be seeking and WHEN they will want that return. For example, a Private Equity investor who invests in more established businesses may be seeking a 3 times return in 5 years on their investment. While a Venture Capital investor, whose investments in startups are riskier, may be looking for a higher 10 times return since they’ll need to balance out the zeros they get on their startups that fail. Your model needs to show how your business will get to your target investors level of return. If your business won’t get there, it’s going to be tough to gain traction with those investors.

Also, you see it actually says Year 5 “+/- 1 to 2 years.” Depending on your type or stage of company, an investor maybe looking to realize their return as early as Year 3 or as last as Year 7. Of course some projects – an infrastructure project for example – may fall outside of this time window. But 5 years plus or minus a year or two is generally what I see the most.

One more thing I want to add here which is about setting expectations – and that is don’t over-promise. I think I want to show return that meets but is not significantly higher than your investor’s target return. You might think the more the better, however, if you set a high bar you’ll have to live up to those expectations later on. Remember that investors are investing for other reasons too such as a great team or product. If your business can demonstrate their target return in the right time frame, I think you have shown what you need to right now. If you think there is significant upside to their target return and you want to highlight that perhaps speak to upside levers or potential that’s not incorporated in the model but available to the business.

Year 10

Finally, let’s look at Year 10. I call this “Change The World” and this is a HUGE vision for the business. Some investors may want to get a sense for how big the business could get especially for startup. And this is where your business will “change the world” 🙂 and what those numbers would look like. I wouldn’t try to show this in the Year 5 numbers. Again, don’t over-promise. And your model doesn’t need to go out this far to Year 10 but rather I would have a metric or two to speak to perhaps a revenue/sales or number of users that you can aspirationally believe you can reach.

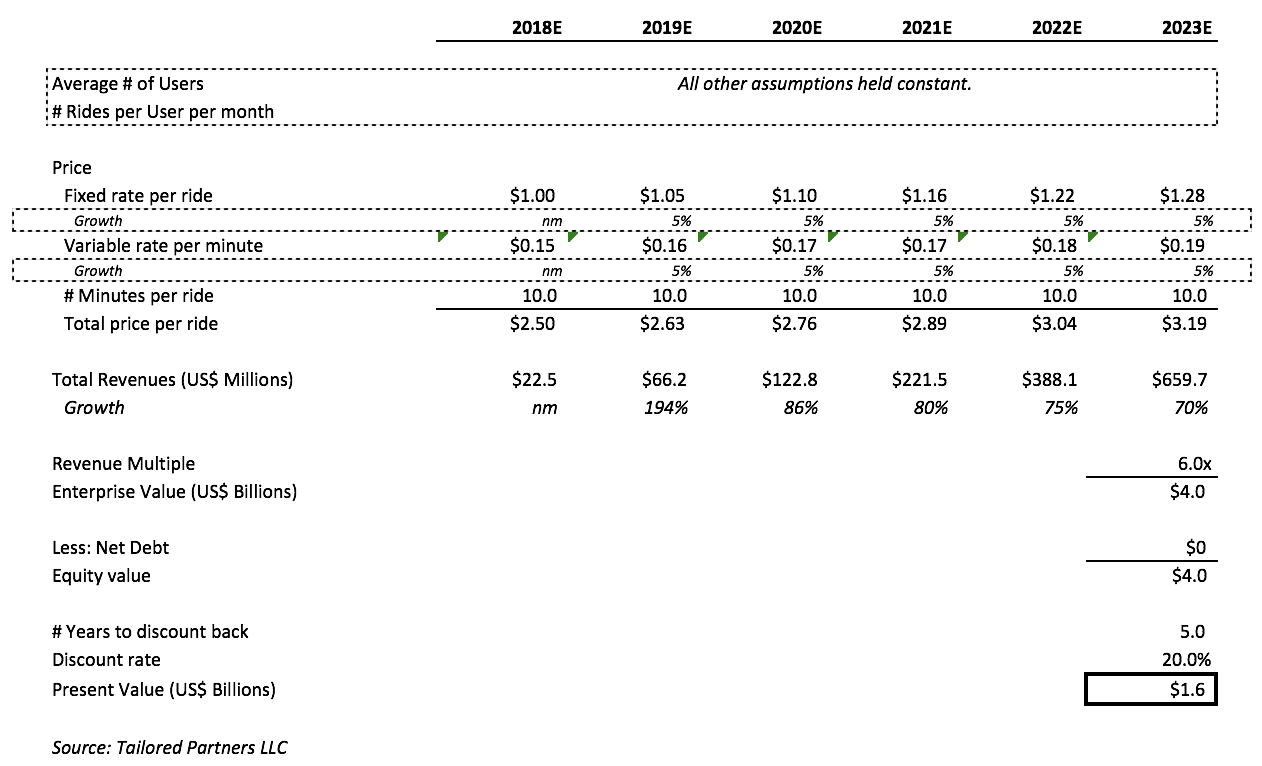

AN EXAMPLE

OK let’s put all this into a quick example! Let’s say you are launching a store to sell electric bikes which are gaining popularity – and you want to launch by raising $500K on a $4M post-money valuation which yields a 12.5% ownership stake for an investor or investor group who we’ll call Investor A.

Example year 1

For Year 1, let’s “Keep It Achievable.” You forecast one ‘small size’ format store with revenues of $150K that’s 300 bikes sold for $500 each or less than a bike a day. An upside lever here to speak to could be that only bike sales are shown so any accessory sales such as helmets will offer upside potential to your numbers.

Looking ahead at the end of Year 1, you expect that you will need to raise again to fund growth. You forecast needing to raise $1M @ 18 months on a $6M post-money valuation which is an 8 times multiple on Year 3 forward revenues of $750K. Investor A is not expected to participate in this round and is diluted to a 10.4% ownership stake.

Example year 2

Looking at the forecasts in this period. In Year 2, you are still just operating one small size store with revenues forecasted to be $300K. That’s +100% year-over-year growth & 600 bikes sold for $500 each and metrics that you could show scale with could be strong revenue growth, customer growth & cash flow break-even at the end of the year.

Example year 3

Looking at Year 3, you have used that new capital to expand your one store to a larger size store which will generate revenues of $750K that’s +150% year-over-year growth & 1,500 bikes sold for $500 each. Metrics showing scale could be accelerating revenue growth, new customer acquisition & being cash flow positive for the full year.

Example year 4

Year 4 is when we plan to “Deliver Results.” At the start of Year 4, you expect that you’ll need to raise again to fund continued growth. You forecast you expect that you’ll need to raise $2.5M at the start of Year 4 on a $16M post money valuation which is an 8 times multiple on Year 4 revenues of $2M. You expect Investor A not to participate again and be diluted down to an 8.8% ownership stake.

For Year 4, you’ve used your capital to expand to 2 stores both at the larger expanded size with a combined. total revenue forecast of $2M. That’s +167% year-over-year growth & 4,000 bikes sold for $500 each. Now revenue growth is driven by volume – not price – in your model so an upside lever available to speak to would be that you could raise prices. Investor A’s 8.8% ownership stake is worth $1.4M yielding a 41% return on their $500K investment. That’s right in line with a 40% return your research shows that they’ll be seeking after 3 years of operations.

Example year 10

Finally, for the investor who wants to see how big this can get, you can speak to the long-term 10-year growth plan the huge vision that you have for the company where you’ll be operating in 3 states by then – NY, CA and TX – which all have 11 cities with 1M+ people. You expect that your branding, locations, people & product strength will create the market leading position and you’ll be operating 15 stores at that time with a revenue forecast at $25M which you believe will expand your multiple to 10X yielding a $250M dollar valuation.

Copyright 2020 Neil Portus | Please see our disclaimers.